The Dividend Investor's Edge Newsletter - February 7th 2022

Volume 3

The Dividend Investor’s Edge is a weekly newsletter designed to give you the investor a full picture of where the stock market is, and to equip you with important information I came across during the week, and what to look for in the week ahead, all constructed in an easy to understand format.

This newsletter is designed for investors of all levels.

Each Week I will discuss:

• An update on the Stock Markets major averages

• Stock Market: On The Horizon

• Notable Upgrades/Downgrades

• Dividend News

📈 Quick Look At The Markets 📉

As a reminder or for those of you new readers, in the “Quick Look At The Markets” section I plan to give you a recap on the prior week for the S&P 500 as a whole as well as the top performing and worst performing sectors. In addition, I will touch on volatility and fear, which are important factors to consider when investing.

With that being said, the stock market had another roller coaster week, but was able to eke out a weekly positive gain. Year-to-date the S&P 500 is still down 5.6%, after gaining 1.6% last week, making that back to back positive weeks.

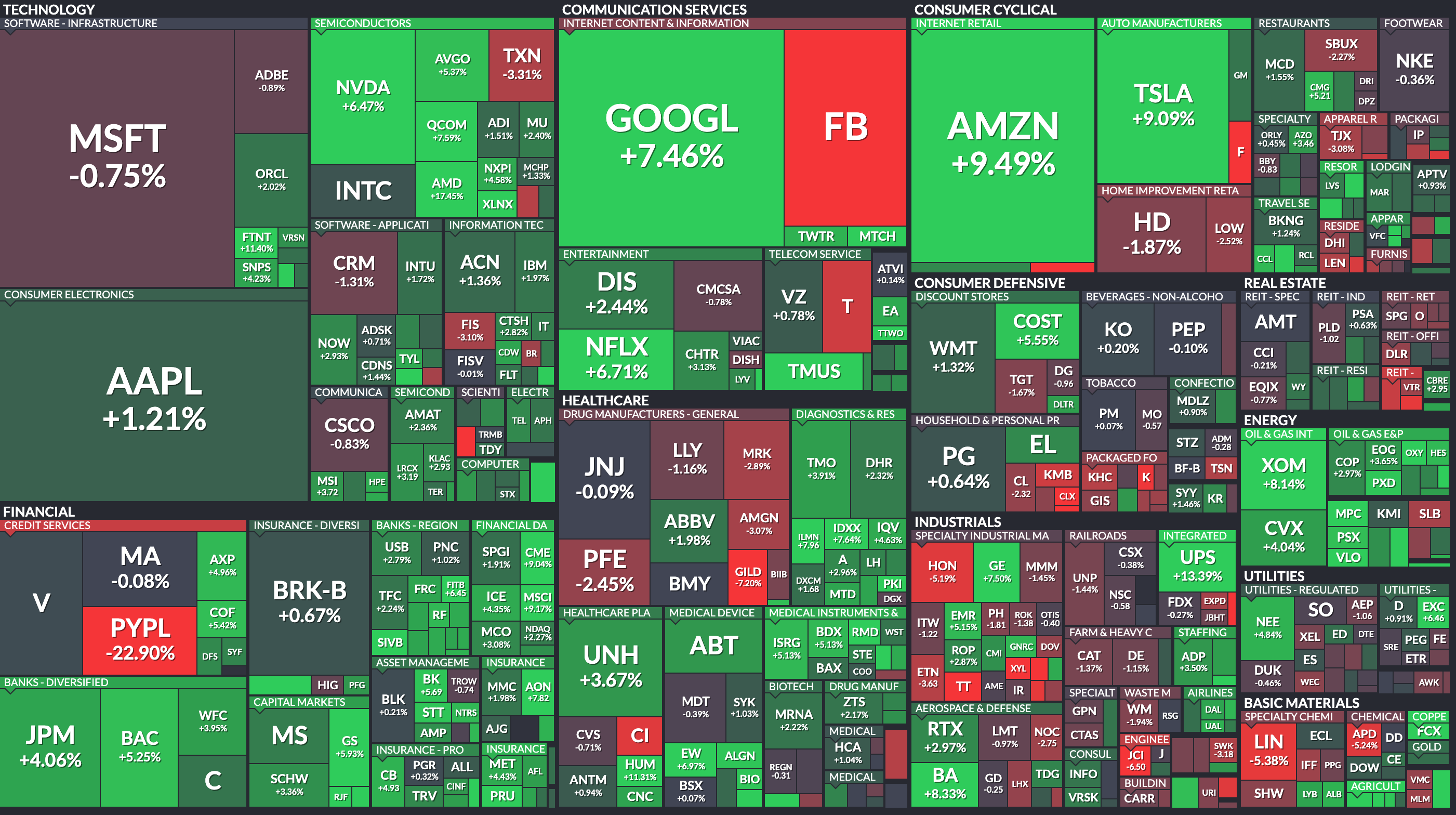

Here is the last weeks heat map for the S&P 500:

Top Sectors For The Week

Energy: 4.94%

Consumer Discretionary 3.94%

Financials 3.51%

Worst Sectors For The Week

Consumer Services -0.25%

Real Estate -0.22%

Materials -0.20%

Fear Factor

Fear levels still remain high, but things did improve as the VIX dropped during the week for the second consecutive week. Volatility levels are coming back towards normal, but that does not mean volatility is gone. We are still in the middle of earnings season, which could bring added volatility so be aware.

Fear and uncertainty is often expressed in the stock market through volatility. One way for investors to understand where the market as a whole is in terms of volatility is by monitoring the CBOE Volatility Index (VIX). The VIX represents the market’s expectations for near-term price changes within the S&P 500 index. The index is derived from index options with near-term expiration dates, projecting a 30-day forward projection.

The VIX ended the week with a reading of 23.22 with the 50-day moving average finishing at 22.45. A reading under 20 is when I consider things to be closer to normal.

Here is a look at the VIX chart with the 50-day moving average:

Another resource you can look at is the Greed and Fear Index that measures market sentiment based on the following seven factors: put/call ratios, junk bond demand, stock price breadth, market volatility, stock price strength, safe-haven demand, and market momentum.

Currently, the index has a reading of 35, which is pretty much flat from prior weeks reading of 36, also indicating higher levels of fear.

📰 Stock Market: On The Horizon 📰

In this section labeled “Stock Market: On The Horizon” I will discuss a variety of different topics that have gone on in the market and are on the horizon.

Last week the markets had a very strong close to the week, finishing up for the second consecutive week after the index saw one of the worst starts to the year in January. During the week, we saw some big moves from stocks that reported earnings. Amazon (AMZN), Alphabet (GOOGL), and Advanced Micro Designs (AMD), were three of the big earnings winners on the week. Paypal (PYPL), Meta Platforms (FB), and Starbucks (SBUX) were three of the top earnings losers on the week, especially the first two, which were both down more than 20% on the week.

In terms of macro news, we did get some decent information in terms of the job market. Weekly initial jobless claims came in at 238,000 compared to an estimate of 2450,000. Nonfarm payrolls came in at 467,000, which was well ahead of the 150,000 estimate.

The nonfarm payroll shows the amount of jobs that were gained during the month, so to hear the 467,000 job gain was a big surprise when we got the news on Friday, which added to fueling the market higher.

The Federal Reserve is still on investors minds especially with the nonfarm payroll numbers we saw on Friday. If you recall from last weeks newsletter, I discussed how rising rates help fight inflation, but the Fed needs to be careful not to bring harm to an economy and its participants. The strong jobs report on Friday gives the Fed more ammo to move forward with their rate hikes, which I expect to begin next month.

This week continues our busy earnings season, but before we look at whose reporting this week, let’s take a brief look at some of the reports from last week.

XOM: The company began in 2022 its $10 billion share repurchase program, which is supposed to play-out over the next 12 to 24 months. The energy space continues to lead the market with oil topping $93 last week.

Adjusted EPS: $2.05, vs. $1.94 expected.

Revenue: $84.97 billion, vs. $84.58 billion expected

PYPL: This was one of the top losers on the week, and although the company does not pay a Dividend, I still like to cover notable earnings calls for you. The company saw total payment volume grow 23% with revenues growing 13% year over year. In addition, PYPL added 9.8 million new accounts. Where things went south for the company is when they issued their 2022 guidance, which was well short across the board. As such, near-term the company is working out some things, but long-term I still like the company to be the “go-to” platform for online purchases.

Adjusted EPS: $1.11, vs. $1.12 expected.

Revenue: $6.92 billion, vs. $6.62 billion expected

AMD: The company reported strong results across the board as well as guidance that shows the growth is not slowing. For FY ‘22, management expects revenue to grow 31% to $21.5 billion and the street was expecting $19.26 billion. AMD continues to be a great holding for those of you looking for semiconductor exposure.

Adjusted EPS: $0.92, vs. $0.76 expected.

Revenue: $4.83 billion, vs. $4.52 billion expected

GOOGL: Alphabet absolutely smashed earnings and investors praised the big-tech firm sending the stock up 7.5% on the week. The company saw big growth in their primary ad business, which includes both search and YouTube, but one of the most talked about items from the earnings release was the company announcing a 20-1 stock split. This is expected to take place on July 15, and for every share of GOOGL stock you own, you will receive 19 more shares. How much you own of the stock will go unchanged in terms of value, as the stock price will be cut as well to line up. Think of it this way, if GOOGL was trading at $20 today and the split took place, and you owned one share. The stock price would be cut to $1/share and you would now own 20 shares, but overall your value is still $20.

Adjusted EPS: $30.69, vs. $27.24 expected.

Revenue: $75.33 billion, vs. $71.83 billion expected

SBUX: Ok, now let’s look at some dividend stocks, and we shall start with a company I have been invested in for years, Starbucks. SBUX has been in the news of late as some of their store employees across the US have been forming unions, which could negatively impact labor costs in the near-term if this progresses. Q1 comps were solid at 13% globally, up 18% in the red-hot US market, but China struggled. Active Starbucks reward members increased 21% YOY as the company now has 26.4 members part of their rewards program. Part of the miss on profit was due to inflation, labor costs, and supply chain issues, which has been a common theme. For me personally, I have been taking this opportunity to add shares to my position.

Adjusted EPS: $0.72, vs. $0.80 expected.

Revenue: $8.1 billion, vs. $7.95 billion expected

ABBV: Many of you know that ABBV is a dividend stock I love dearly as it has strong cash flows, a high yield, and a growing dividend. The company reported solid earnings and guidance for the year ahead. Humira, which has long been the top selling drug in the world, saw revenues grow 3.5% during the quarter, with US Humira sales growing 6%. Skyrizi and Rinvoq are two up and coming drugs that have seen robust growth. Check out my latest detailed write-up on AbbVie in my article titled, “AbbVie Stock: Get In On This Investor Trifecta.”

Adjusted EPS: $3.31, vs. $3.28 expected.

Revenue: $14.89 billion, vs. $15.59 billion expected

QCOM: Qualcomm was an interesting stock last week because the company reported solid earnings plus guidance that surpassed analysts expectations, yet shares fell more than 4% the following day. In reading up on multiple analysts reports, the fall was not so much due to the earnings from this quarter, but for what is to come, particularly when it comes to chip sales for smartphones. They are expecting a stronger than normal decline as Apple has moved to their own chip and Android is moving to more of a mid-tier modem chip, which will present headwinds for the company. However, my take is that the company is trading at a very reasonable valuation, suggesting that this is already built into the stock price. I do not own shares, but I do own options.

Adjusted EPS: $3.23, vs. $3.00 expected.

Revenue: $10.7 billion, vs. $10.43 billion expected

AMZN: Amazon, although another non-Dividend paying stock, crushed earnings during their holiday period. They reported strong numbers from AWS and they also hiked the price of their popular Amazon Prime subscription. In case you were not aware, AMZN had a sizable ownership in EV maker Rivian prior to them going public, and they recently cashed out some of that ownership recording an $11.8 billion gain during the quarter. Supply chain issues combined with labor and transportation issues continue to be a short-term headwind for the company. Shares gained 13.5% after earnings.

Adjusted EPS: $27.75 ($4.82 w/o Rivian sale), vs. $3.54 expected.

Revenue: $137.4 billion, vs. $137.17 billion expected

BMY: Bristol-Meyers reported both earnings and guidance that was pretty much in-line with what the street was looking for. The company continues to have one of the strongest portfolio of products and pipelines in the industry and they trade at a sizable discount in my opinion. Management announced a $15 billion share repurchase program with a $5 billion accelerated share repurchase program to take place in the first quarter. I have a large stake in BMY and continue to add on any pullbacks, which have not been happening of late as the stock has been running after trading in the mid-$50s a few months back.

Adjusted EPS: $1.83, vs. $1.80 expected.

Revenue: $12 billion, vs. $12 billion expected

This week is also jam packed with another round of important earnings results. Here is a look at companies that are reporting earnings this week (via @eWhispers).

Notable Earnings Calls I am watching closely:

SPG

PFE

CVS

DIS

KO

PEP

Here are some key data reporting due this week:

2/10: CPI

2/10: Continuing Jobless Claims

2/10: Initial Claims

2/11: Michigan Sentiment report

It will yet again be another jam packed week of reports and data to go through, but that is part of the reason I put this newsletter together, so you can have a one stop shop for important market news and data.

The plan in the week ahead is to continue looking for opportunities in high-quality companies that have established businesses and are turning positive cash flows. Disney will be a closely watched stock for me as I will look to add to my position on any weakness, as I believe in them long-term and also believe I will see the dividend again some day.

⏫ Stock Upgrades/Downgrades ⏬

In this section moving forward, I will add any notable analyst Upgrades or Downgrades I came across during the previous week.

Mastercard (MA) PT increased to $435 from $400 at Mizuho

Visa (V) PT increased to $235 from $220 at Mizuho

AbbVie (ABBV) PT raised to $150 from $133 at Barclays

Starbucks (SBUX) PT lowered to $116 at Deutsche Bank

💰 Dividend News

In this section I will detail what I am watching and any Dividend related news.

United Postal Service (UPS) increased their dividend by 49%

Other Resources

Here are a few of my latest YouTube videos to watch:

3 Dividend Stocks To Buy In February 2022

Top Dividend Aristocrats To Buy Now

If you do not already follow me on social media, give me a follow as I put out weekly content.

Thank you for reading my newsletter! Please comment down below and share the newsletter with someone that may find it useful. Also, message me and let me know what you think of the newsletter and anyway I could improve it going forward. You can email me directly at Mark@RoussinFinancial.com.

Have a Great Week!

Mark